Synopsis

This article tests the common belief that the Ministerial Housing Allowance is a major tax windfall for pastors. The process ran dozens of 2017 and 2025 tax scenarios, comparing pastors with similarly paid regular employees. It shows that once SECA and today’s higher standard deduction are factored in, many pastors now pay roughly the same—or even more—total federal tax than their lay counterparts, while only some higher‑paid pastors with large housing costs see significant savings. The results for pastors who earn:

- Under $100,000: often neutral to negative.

- $100,000–$150,000: marginal benefit, depending on spouse income and housing.

- $150,000+: meaningful benefit possible, if one has high housing costs.

Itemizing can change your tax scenario. You can download this article as a PDF here..

Introduction

A church elder in SoCal was talking with me about the results of an XPastor Compensation Study. The elder said, Our pastoral salaries might be a bit lower, but pastors have the housing allowance … and that is a boon for their salaries. Most pastors and board members think that there is great tax benefit from the Ministerial Housing Allowance. Is that true?

While I had studied the benefit of the Ministerial Housing Allowance in 2017, it was time for a new investigation. The results may shock you. In the words of the SoCal elder to these findings: This is helpful and sad at the same time.

The challenge of writing this article is the large number of variables concerning pastoral salary, spouse regular employee salary and housing expenses. For 2025 salaries, I created 50 unique scenarios with TurboTax. Your mileage will vary with your income and expenses.

The following only pertains to federal income taxes. Your taxes may be higher if you pay state or local taxes. Your taxes may be lower if you can itemize your deductions.

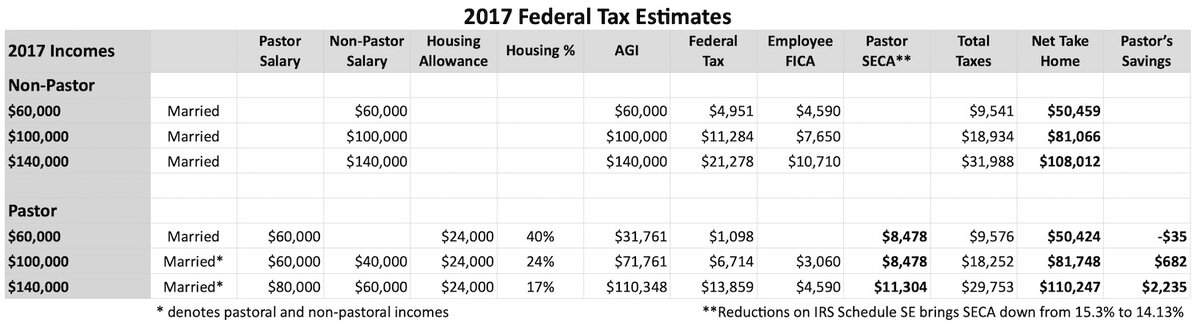

2017 Taxes

In 2017, I studied 10 salary scenarios concerning the housing allowance. Compared to a regular employee who pays FICA:

- A pastor with a $60,000 salary with a non-earning spouse, and a $24,000 housing allowance, owed $35 more.

- A pastor with a $60,000 salary with a regular employee spouse earning $40,000, and a $24,000 housing allowance, saved $682.

- A pastor with a $80,000 salary with a regular employee spouse earning $60,000, and a $24,000 housing allowance, saved $2,235.

A great many pastors in 2017 either lost $35 or gained $682. A few well-paid pastors with working spouses saved $2,235. Those are ranges from -.05% to +1.60% of their total salary. The tipping point was at about $60,000 in salary. In 2017, the Ministerial Housing Allowance was not a boon for pastors.

Remember SECA

Ministers wear two hats with the federal government.

- For income tax reporting, pastors are employees and so receive a Form W-2 Wage & Tax Statement, with the housing allowance excluded from Box 1.

- For tax purposes, pastors are self-employed.

These two hats bring plenty of confusion. The pastor pays Social Security and Medicare according to the Self-Employment Contributions Act (SECA). The SECA rate is 15.3%.

Regular employees in churches and businesses pay FICA. For Social Security and Medicare, the employer pays 7.65% and the employee pays 7.65%. The employer’s portion of FICA is a business expense and not shown on Form W-2 or considered part of salary. It is essentially hidden to the employee. It’s just a cost of doing business. The employee portion of FICA is included on Form W-2, but not included in the total tax number on Form 1040, Line 16

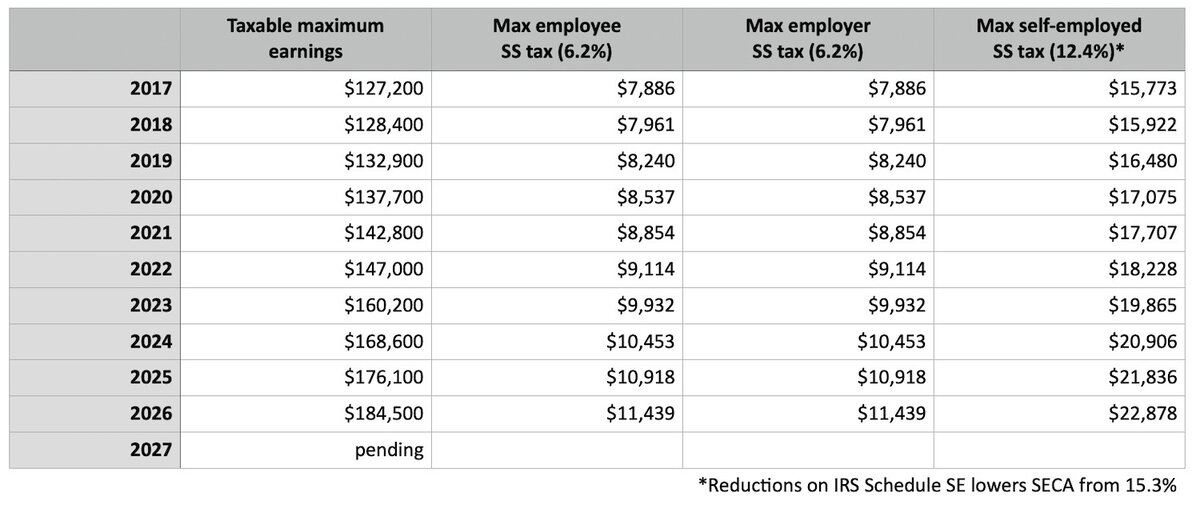

Consider the costs of SECA for the pastor. For Social Security and Medicare, the pastor pays the employer portion (7.65%) and the employee portion (7.65%). To find your SECA percentage, don’t multiply your salary by 15.3%. There are reductions on Schedule SE that brings the SECA percentage down to an effective rate of 14.13%. Here is the SECA tax for pastors earning less than $176,100 in 2025.

- For a $60,000 pastoral salary, SECA is $8,478.

- For a $93,000 pastoral salary, SECA is $13,141.

- For a $140,000 pastoral salary, SECA is $19,782.

SECA is paid on total salary, including the Ministerial Housing Allowance. To be a benefit, the Ministerial Housing Allowance needs to lower the pastor’s federal income tax bill by about half of those SECA dollars.

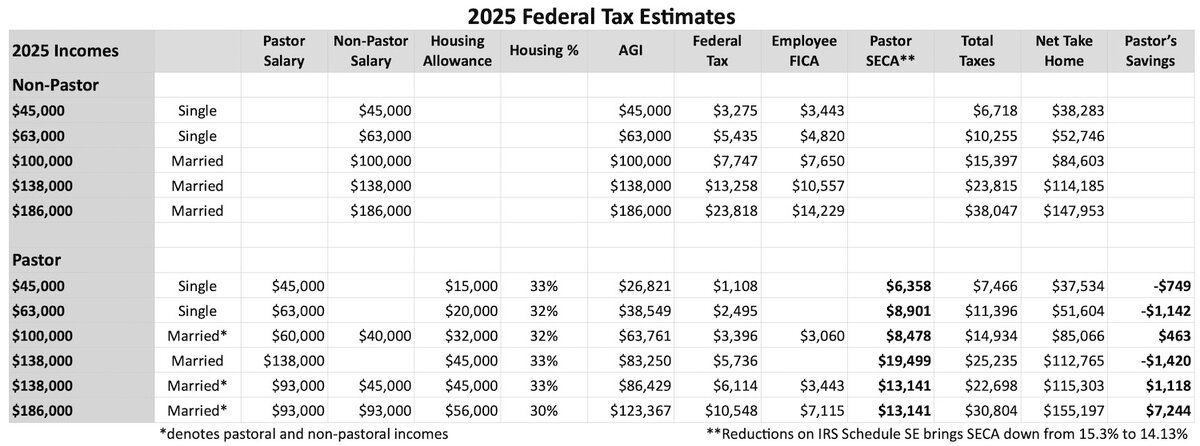

2025 Taxes

Having studied the Ministerial Housing Allowance in 2017, I returned to the study in 2025. Things drastically changed. Back in 2017, the married standard deduction was $12,700 and by 2025 rose to $31,500.

That means in 2025, most pastors didn’t itemize deductions on Schedule A of the federal tax form. Before 2018, pastors often used to double dip by itemizing and getting the Ministerial Housing Allowance. Now, most pastors take the standard deduction like regular employees. That changes the tax game. A few salaries in 2025 tell the tale. Compared to a regular employee who pays FICA:

For Most Households

- A non-married pastor earning $63,000 with a $20,000 housing allowance owed $1,142 more.

- A pastor with a $60,000 salary with a regular employee spouse earning $40,000, and a $32,000 housing allowance, saved $463.

For High Wage Earning Households

- A pastor with a $93,000 salary with a regular employee spouse earning $45,000, and a $45,000 housing allowance, saved $1,118.

- A pastor with a $138,000 salary with a non-earning spouse, and a $45,000 housing allowance, owed $1,420 more.

- A pastor with a $93,000 salary with a regular employee spouse earning $93,000, with a $56,0000 housing allowance, saved $7,244.

There are a myriad number of variations of pastoral salary, regular employee salary and housing expenses. A great many pastors in 2025 either lost $749 or gained $1,119. A few well-paid pastors with working spouses saved $7,244. Those are ranges from -1.81% to +3.89% of total salary. While a nice break for some, that’s not a boon for pastors.

The more you earn, the higher the SECA tax, up to the Social Security salary cap of $176,100 in 2025—Medicare is not capped. The more you spend on housing, the more you may save on total federal taxes. If you are a high earner, and spend a great deal on housing, then you may be saving money with the Ministerial Housing Allowance.

In 2017, the tipping point for saving money with the Ministerial Housing Allowance was about $60,000 in pastoral salary. In 2025, the tipping point for saving taxes is about $150,000—that is a rough number as the issues become complicated with single versus two earner households, various Housing Allowances and those 9.34% of tax filers who itemize on Schedule A.

Do-It-Yourself Ideas

Are you curious how your SECA pastoral salary compares with a FICA regular employee? You can compare your pastoral salary with SECA to a regular employee who pays FICA in six steps:

- Make a copy of your 2025 tax software file and title it Regular Employee:

- Put your total salary including housing allowance into Box 1 of the tax program’s Form W-2.

- Put your total salary in Social Security wages in Box 3 of Form W-2 and multiply your salary by 6.2% for Box 4, Social Security Tax withheld. If you make more than the $176,100 cap in Social Security taxation of pastoral income, then you will need to have your tax software help you with the exact amount.

- Do the same for Boxes 5 & 6 for Medicare but multiply your salary by 1.45%. The $176,100 cap does not apply to Medicare.

- Delete all references to being a pastor in the following W-2 Information Screens. Delete any reference or numbers in the Ministerial Housing Allowance sections.

- Look at the tax paid on the IRS form 1040, line 16. Add to that combined Form W-2 FICA amounts (Social Security from Box 4 and Medicare from Box 6) paid by a regular employee. You add that in because Form 1040 does not include employee FICA in the income tax summary. The regular employee has paid it through payroll deductions. That combined number is the total tax paid by a regular employee.

This exercise may take you 30 minutes. Your mileage will vary. For example, in discussing this article with a pastor, I helped him determine his savings or loss. In TurboTax, we ran his salary of $240,000 in ministerial income and $10,000 in spouse regular income. We included his $50,000 housing allowance. With a total family income of $250,000, he lost $141 compared to a regular employee earning the same amount.

Solutions

Change Pastors to Regular Employees

Congress could enact legislation to eliminate the Ministerial Housing Allowance and make pastors regular employees. Such an act might elate many of the 500,000 Christian pastors and others—such as Rabbis, Imams, and Native American Traditional Healers.

Such legislation would create budget havoc for the 370,000 churches in the U.S. and other houses of worship—such as Synagogues, Temples, Mosques, and Native American governing bodies. Each religious congregation would have to pay FICA at 7.65% for their pastors or other ministerial workers. For example, a church with $1,000,000 in pastoral salaries would pay $76,500 in FICA.

Give a FICA-Type Bonus

About 20-30% of churches give a FICA-type bonus to pastors. The bonuses range from 2% up to 17%, with the average being about 8.0%. A FICA-type bonus may be the wave of the future to help pastors and others pay the disproportionate cost of SECA and deal with the diminished value of the Ministerial Housing Allowance. As a bonus, this income is subject to federal income tax and SECA. A bonus can be given immediately, at the end of the calendar year or in each paycheck.

For example, consider a church that wants to help their pastors with SECA tax imbalance. The board resolves to immediately give a taxable FICA-type bonus of 3% to their pastors. The church board also decides that in the next fiscal year the bonus will rise to 5%, be paid in each paycheck and be a part of their General Fund budget. In the third year they hope to raise the bonus to 7% and cap it at 9% in the fourth year. The board deemed that this multi-year rollout would be doable for their budget, spreading out the increases over four years.

The FICA-type bonus would begin helping pastors in the first year and will be of maximum help in the fourth year. In this example, the pastors would be elated!

Conclusion

As this article shows, this is a complicated topic. Use the DIY section to run your own numbers or rely on the samples given. Your mileage will vary with your income and expenses when applying the Ministerial Housing Allowance.

The changes in the Standard Deduction in the Tax Cuts and Jobs Act of 2018 had a dramatic effect on the tax savings for pastors from the Ministerial Housing Allowance. The allowance was never a boon for pastors, but before 2018 it had some savings for most pastors. In the current tax structure with higher Standard Deductions, the Ministerial Housing Allowance helps some highly-compensated pastors who have high housing expenses.

Some churches may decide to keep Directors as regular employees, instead of licensing or commissioning them into pastoral roles. Others who do commission Directors will want to carefully explain the tax consequences of the decision. All new pastors will need a great deal of education on this topic. Note that once you are a pastor, you can’t go back to being a regular employee if you are doing the same role.

There is tax savings when a spouse works as a regular employee. While this raises the total federal income tax, it allows the pastor to spend more on housing. However, if the couple doesn’t have much in housing expenses, then they are going to lose money!

One also needs to remember other costs with the Ministerial Housing Allowance:

- Time by the pastor to assemble a Ministerial Housing Approval sheet.

- Time by the Board to review and approve the Ministerial Housing allowance.

- Work by the accounting department in having two types of employees—pastors and regular employees.

- Effort a pastor puts into filling out the Form 1040 with the correct Form W-2 information and ministerial housing information.

Chris Purnell, Partner and Tax Counsel at CRI CapinCrouse said:

The amount you get paid matters. The amount of housing allowance that is designated and therefore, excluded from income tax really matters, though there is a push and pull there, as the minister will still often lose on the SECA side of things. Ministers need to be educated about this!

Emily VerSteeg, Vice-President at ECFA said:

We think the article is on point overall. As tax laws change, the housing allowance may no longer be as valuable as it once was. However, everyone’s tax situation is different, and the article points this out. Adding the FICA bonus or another financial benefit to offset the potential loss of value from the housing allowance is a good suggestion.

The education provided to the board in this article is excellent, as so many board members do not understand housing allowance. This provides the CFO the support he needs to assist a pastor with the cost of SECA.

Now that you have been educated, share this with other pastors and the church board. What is seen as a boon for pastors is either costing pastors money or saving money for a few.

More churches should consider a FICA-type bonus to help pastors offset the loss caused by the Ministerial Housing Allowance.

After reading this article, send comments to me—I want to hear from you.

Peer Review

Due to the complexity of these issues, the following did a peer review:

- The Evangelical Council for Financial Accountability

- Chris Purnell, Attorney—Partner and Tax Counsel at CRI CapinCrouse

- Tim Samuel, CPA—Chief Financial Officer at Bridgeway Community Church

Appendix 1—Federal Tax Estimates for 2017 & 2025

Appendix 2—Changes to Itemized Deductions

Can a pastor itemize on Schedule A? The answer is perhaps. The value of the Ministerial Housing Allowance is focused on reducing taxable salary. The starting point to answer the question is in the standard deduction rate.

In the last ten years, standard deduction rates have risen substantially. From 2017 to 2018, they went up 89%. From 2017 to 2026, they rose 153.5%.

Because of the higher standard deduction rate, most pastors no longer itemize on Schedule A. The result is that the housing allowance saves little federal income tax, but SECA applies to the pastor’s total salary.

This rise in standard deductions in 2018 led to a steep decline in the number of people who itemized on Schedule A.

For tax year 2017, the IRS reports there were 143,300,000 individual income tax returns. Of those, 46,745,648 claimed itemized deductions on Schedule A. That is 32.62% of all returns filed that year. This was before the Tax Cuts and Jobs Act changes took effect for 2018.

The most recent IRS Statistics of Income tables go through tax year 2021. For 2021, there were 160,392,132 individual income tax returns. Of those, 14,974,757 claimed itemized deductions on Schedule A. That is 9.34% of all returns filed that year.

The decline in the number of pastors filing Schedule A took away a significant tax benefit. The standard deduction rate helped regular employees. For most pastors, the result was an erosion of the benefit of the Ministerial Housing Allowance.

Appendix 3—IRS Regulations

Here are excerpts from IRS Publication 517, Social Security and Other Information for Members of the Clergy and Religious Workers:

Ministers

If you are a minister of a church, your earnings for the services you perform in your capacity as a minister are subject to SE tax, even if you perform these services as an employee of that church.

Ministers are individuals who are duly ordained, commissioned, or licensed by a religious body constituting a church or church denomination. Ministers have the authority to conduct religious worship, perform sacerdotal functions, and administer ordinances or sacraments according to the prescribed tenets and practices of that church or denomination.

If a church or denomination ordains some ministers and licenses or commissions others, anyone licensed or commissioned must be able to perform substantially all the religious functions of an ordained minister to be treated as a minister for social security purposes.

Even though all of your income from performing ministerial services is subject to self-employment tax for social security tax purposes, you may be an employee for income tax or retirement plan purposes in performing those same services.

The Self-Employment Tax Exemption

File Form 4361. File by the due date of your income tax return for the second tax year in which you had at least $400 of net earnings from self-employment, any of which came from ministerial services. You are conscientiously opposed to public insurance because of your individual religious considerations (not because of your general conscience), or you are opposed because of the principles of your religious denomination. You file for other than economic reasons (meaning: you can’t file the exemption for economic reasons. Editor).

Housing Designation

The church or organization that employs you must officially designate the payment as a housing allowance before it makes the payment. It must designate a definite amount. It can’t determine the amount of the housing allowance at a later date. If the church or organization doesn’t officially designate a definite amount as a housing allowance, you must include your total salary in your income.

An official designation of an amount as a housing or rental allowance may be shown in an employment contract, in the minutes of a church or qualified organization, in a budget, or in any official action taken in advance of payment of the allowance. A designation is sufficient if it permits a payment to be identified as a payment of a rental or housing allowance as distinguished from salary or other remuneration. Informal discussions don’t amount to an official designation.

Retired Ministers

If you are a retired minister, you can exclude from your gross income the rental value of a home (plus utilities) furnished to you by your church as a part of your pay for past services, or the part of your pension that was designated as a rental allowance. However, a minister’s surviving spouse can’t exclude the rental value unless the rental value is for ministerial services they perform or performed.

Deduction for SE Tax

You can deduct one-half of your SE tax in figuring AGI. This is an income tax deduction only, which is claimed on Schedule 1 (Form 1040), line 15.

Estimated Tax

The federal income tax is a pay-as-you-go tax. You must pay the tax as you earn or receive income during the year.

Appendix 4—Maximum Social Security Taxable Rates